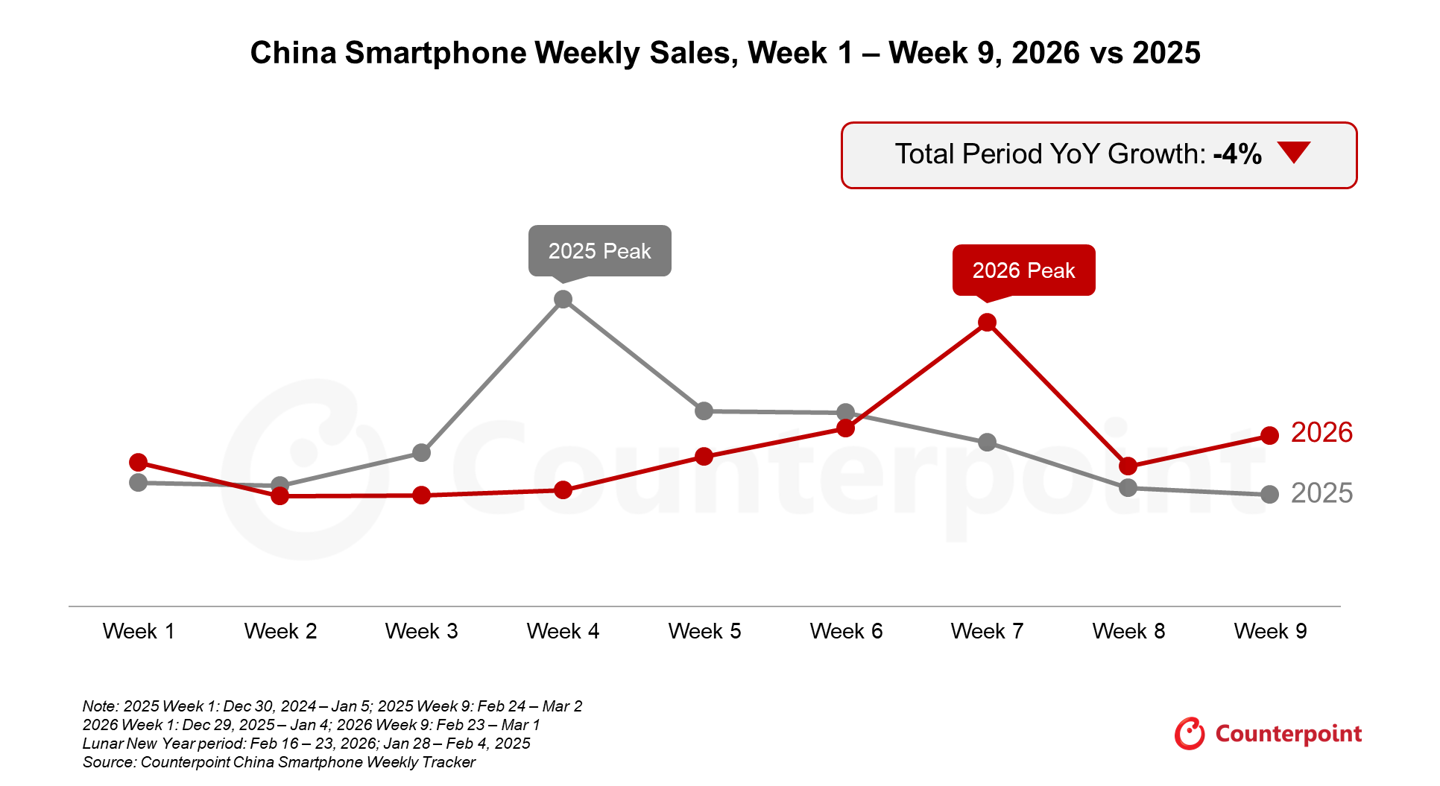

CounterPoint Research says China’s smartphone market got off to a weak start in 2026, with sales down 4% year over year during the first nine weeks of the year. The firm says soft overall demand and sharply higher memory chip prices were the main forces dragging the market lower.

The report notes that sales did improve in February during the Lunar New Year promotion window compared with January, so the market didn’t stay flat the whole time. Even so, the rebound wasn’t strong enough to offset the broader pressure building underneath the industry.

One major problem is cost. According to the report, rising memory prices have severely limited how aggressively phone brands can cut prices. During the 2026 holiday promotion period from February 16 to 23, overall smartphone sales across major brands were still down 2% from a year earlier, which meant the seasonal campaign underperformed compared with last year’s result.

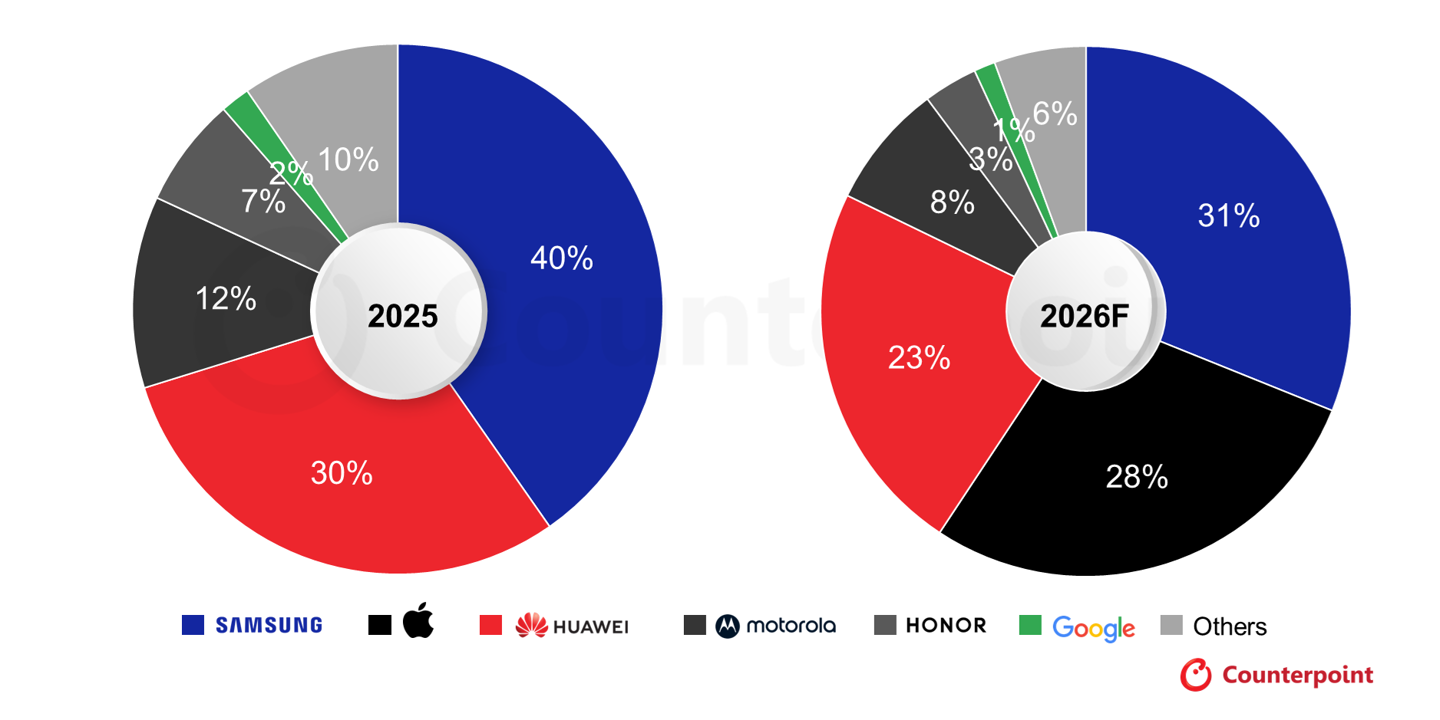

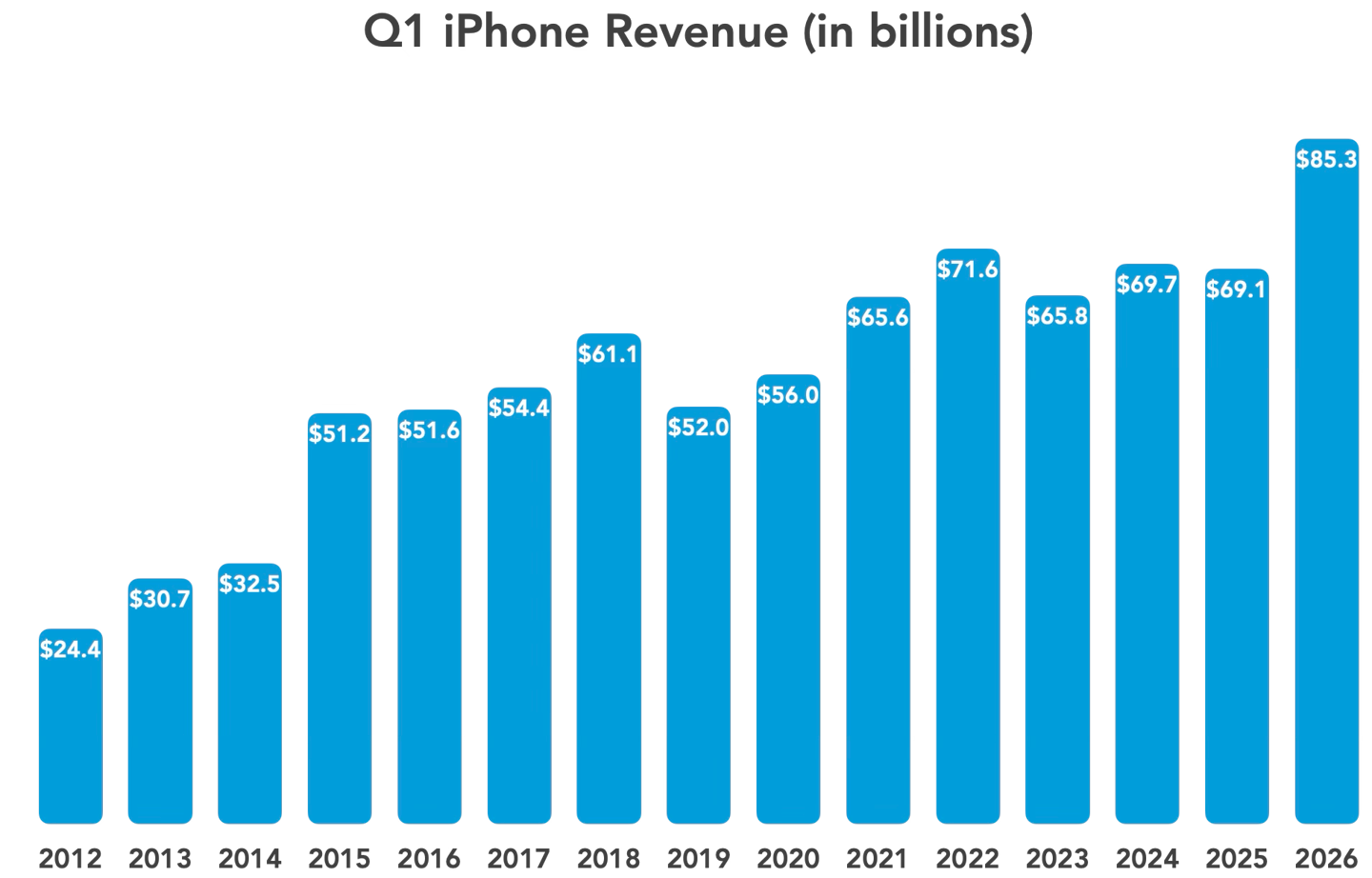

That cost pressure appears to be hitting Android vendors harder. The report draws a sharp contrast between those brands and Apple, which it says posted a 23% year-over-year jump in China sales over the first nine weeks. Apple China demand was reportedly helped by e-commerce discounts as well as strong sales of the base iPhone 17 model.

CounterPoint argues that Apple’s control over its global supply chain gives it more room to absorb part of the margin squeeze on its own. Because of that, the firm expects Apple to avoid fully following the latest round of price increases, which could give it an opening to expand share further while competitors remain under more strain.

Huawei was also flagged as relatively well positioned. The report says the company has an important cost buffer because it relies more heavily on lower-cost domestic memory suppliers. In an environment where global component prices are rising, that could help Huawei move more aggressively in the midrange and entry-level market.

Looking ahead, CounterPoint Research expects the China smartphone market to stay under pressure from March through May. The firm says the next realistic point for a meaningful rebound may be the 618 shopping festival in early June. Until then, the market is likely to keep dealing with the same mix of weak demand and elevated component costs.

Just as importantly, the report suggests the spike in memory chip prices is not a short-lived issue. Instead, it sees the higher-cost trend as something that will probably run through all of 2026, which could keep reshaping pricing strategy and competition across the broader China smartphone market.