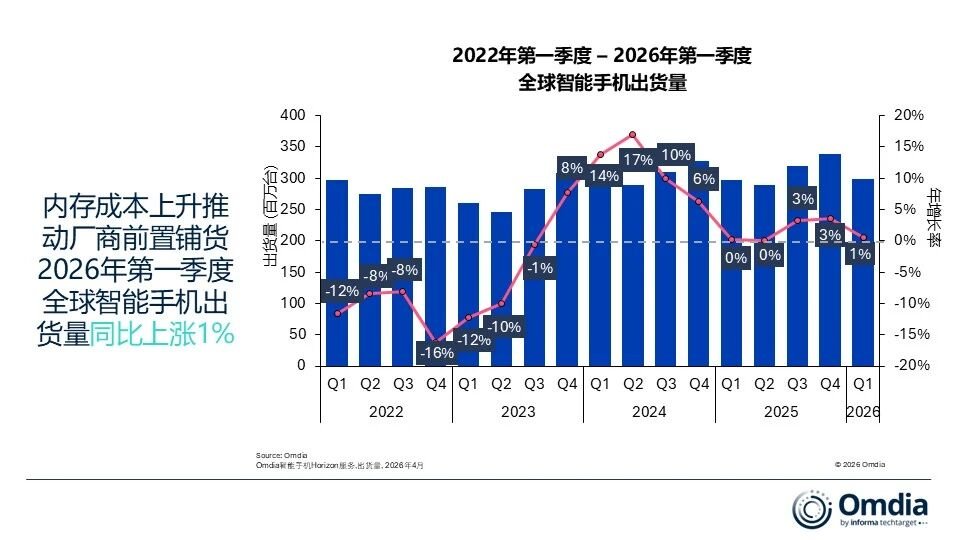

Market research firm Omdia says global smartphone shipments reached 298.5 million units in Q1 2026, up 1% year over year. That result came in better than many early expectations, but the report also makes it clear that the apparent strength at the start of the year doesn’t necessarily mean the market is on solid footing for the months ahead.

According to Omdia, the first quarter was shaped by two forces moving in opposite directions. On one side, major brands including Samsung and Apple pushed more product into channels earlier than usual because they expected higher memory and component costs later on. That front-loaded activity lifted shipment totals. On the other side, weak macroeconomic conditions kept pressure on real consumer demand, with high living costs squeezing discretionary spending and widening the gap between channel shipments and actual retail sell-through.

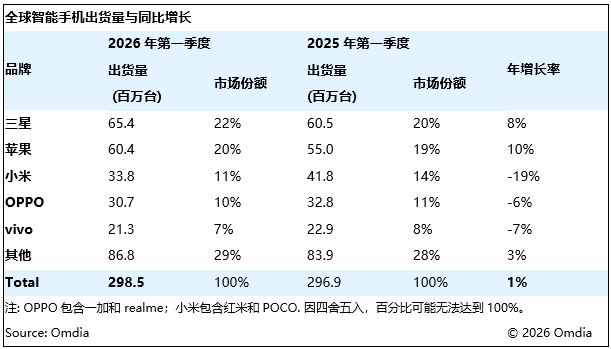

Samsung held onto the top spot globally in the quarter, shipping 65.4 million smartphones for 8% annual growth. Omdia says the company benefited from a two-track lineup strategy: entry-level Galaxy A models stayed resilient in emerging markets, while strong sales from the Galaxy S26 family supported the premium end.

Apple ranked second with 60.4 million shipments, up 10% year over year. The report points to the iPhone 17 series as the main growth engine, while also noting that the newer iPhone 17e opened strongly in carrier-led markets such as the European Union and Japan. Omdia adds that first-wave sales of the iPhone 17 Pro and Pro Max outperformed the prior generation, with mainland China highlighted as an especially strong market.

Xiaomi shipped 33.8 million units in the quarter, down 19% from a year earlier and marking the steepest decline among the top five brands. Omdia says more than half of Xiaomi’s shipments were concentrated below the $200 segment, leaving the company more exposed to rising memory costs and tighter margins in the value tier.

OPPO, including realme and OnePlus, placed fourth with 30.7 million shipments, down 6%. vivo came in fifth with 21.3 million units, down 7%. Omdia ties those declines partly to aggressive entry-level channel stocking late in 2025, followed by slower end-market sell-through in the opening quarter of 2026.

Outside the top five, Honor was one of the brighter spots. Omdia says the brand posted 19.2 million shipments and 19% year-over-year growth, making it the fastest-growing name among the global top ten smartphone vendors. Overseas momentum, especially in the Middle East and Africa, played a major role, even as competition at home weighed on its mainland China performance.

The broader takeaway from the report is that the market may be entering the early phase of a supply-driven disruption cycle. Omdia argues that rising prices for memory, storage, processors, and other core components are prompting brands and channel partners to lock in orders early and build up inventory before costs climb further. That strategy can temporarily inflate shipment numbers, but it also raises the risk of excess stock later on.

At the same time, Omdia says real consumer demand remains fragile. Inflation in everyday essentials is still forcing buyers to stretch replacement cycles and spend more cautiously, with mid-range and premium phones facing softer demand in many cases. The report also warns that lower-end devices are under special pressure because their profit buffers are thinner and price-sensitive buyers react more quickly when component costs are passed through.

Omdia research manager Le Xuan Chiew says the first-quarter data mainly reflects short-term supply-side distortion rather than a clean demand recovery. In that view, concentrated pre-stocking by brands and channels boosted headline shipments, but elevated inventory levels are likely to weigh on later quarters as the market works through that stock.

Looking ahead, the firm expects the industry to shift from short-term expansion into a deeper adjustment phase. Omdia says the second quarter of 2026 could mark the start of a broader inventory correction, while the pace of any recovery is likely to be uneven and weaker than earlier hopes suggested.

The report adds that rising memory costs may become even more visible in the second half of the year, further eroding consumer purchasing power and extending upgrade cycles. In response, smartphone makers are expected to focus more on controlling channel shipments, reducing inventory risk, and protecting baseline profitability. In other words, Omdia sees a market where shipment discipline may matter more than aggressive expansion for the rest of 2026.