According to the latest smartphone market outlook tracker report from global research firm Counterpoint, the global smartphone industry is entering a severe period of downward adjustment.

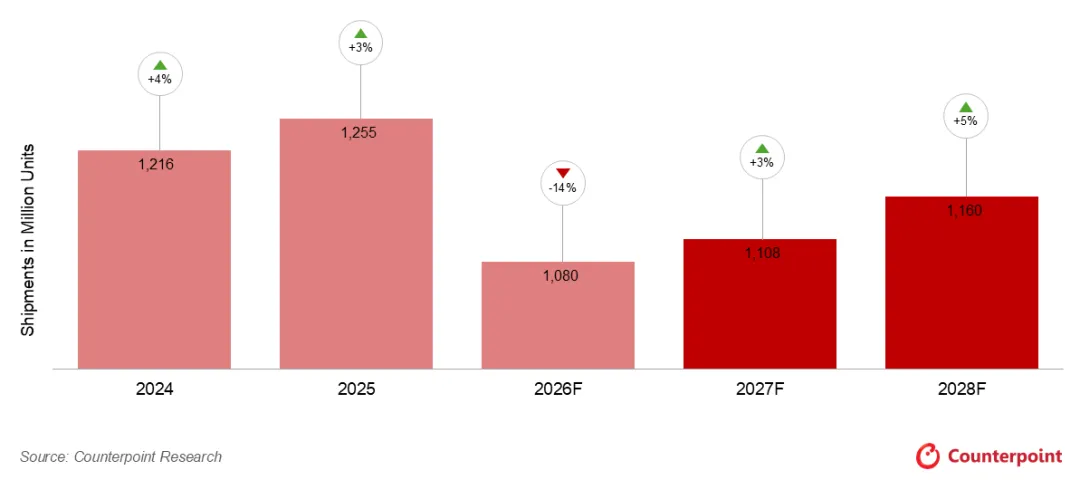

In its updated forecast, Counterpoint projects that global smartphone shipments 2026 will tumble by 13.9% year-on-year to approximately 1.08 billion units. This marks a historic low since 2013, representing a steeper decline than the 12.4% contraction previously estimated in February.

The primary driver behind this sharp market downturn is a severe and persistent memory supply shortage. Semiconductor manufacturers have been shifting their production capacity away from standard mobile RAM to meet the explosive demand for High Bandwidth Memory (HBM) and server DRAM in the AI sector. As a result, LPDDR4 and LPDDR5 prices are expected to double in the second quarter of 2026 compared to late 2025. Given the high capital requirements and long lead times of chip fabrication, this smartphone market memory shortage is expected to drag on until the second half of 2027.

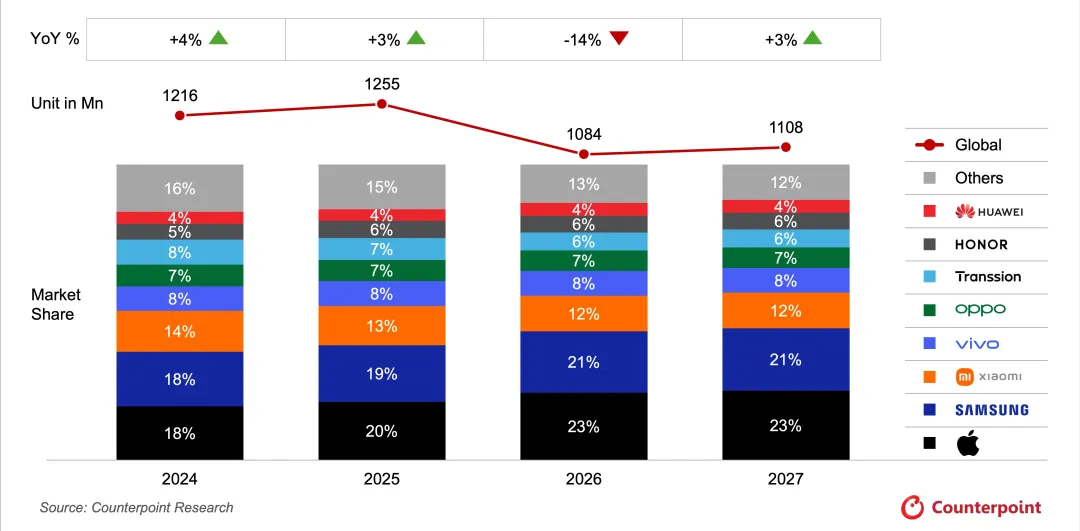

Premium OEMs like Apple and Samsung are relatively insulated from the crunch. Apple’s iPhone shipments are expected to remain stable in 2026 before growing 5% in 2027, while Samsung’s annual shipments are projected to dip by just 4%. Meanwhile, Huawei stands out as the only major Chinese brand forecast to achieve shipment growth in 2026.

In contrast, budget-focused smartphone manufacturers and emerging markets are bearing the brunt of the supply shock. Mobile LPDDR4 supply is expected to plummet by over 40% in 2026, sending wholesale device prices up by 14% in the first quarter of the year. As cheap, legacy components are depleted, the budget smartphone market decline will accelerate, leaving devices priced under $150 at risk of being completely squeezed out of the market.

Fortunately, industry analysts expect a strong recovery to begin in 2028. This eventual rebound will be driven by stabilizing chip supply, pent-up consumer demand, and the rollout of 6G networks in early adopter markets like China, Japan, and South Korea, alongside a mature ecosystem of AI-native hardware.