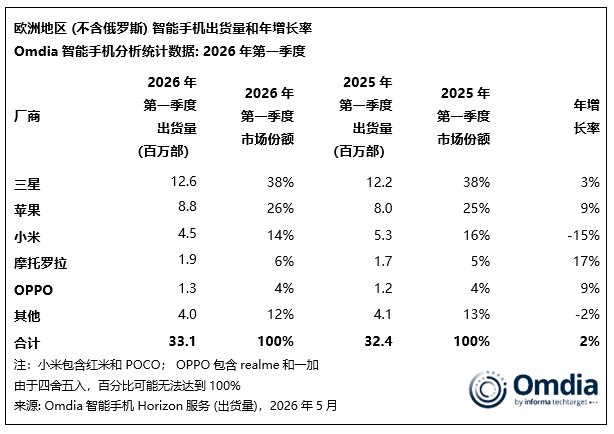

Europe smartphone prices reached a new high in the first quarter of 2026, according to fresh research from Omdia. The firm said the smartphone market in Europe, excluding Russia, grew 2% year over year to 33 million units, showing some resilience even as supply chain costs kept rising and product availability risks stayed in the picture.

Omdia said the market was helped by steady end-user demand and by channel partners stocking inventory earlier than usual. Even with those tailwinds, the report suggested the market backdrop is still uneasy, especially as memory costs continue moving up.

Samsung remained the top smartphone vendor in Europe during the quarter, shipping 12.6 million units for 3% annual growth. Omdia linked that result in part to effective promotions around the Galaxy A16 4G, which helped offset delays affecting the Galaxy S26, A57, and A37 launches.

Apple ranked second with 8.8 million units shipped, up 9% from a year earlier. The report said strong demand for the iPhone 17 lineup and broader mid-range coverage from the iPhone 15 and iPhone 16e supported that gain. Omdia also noted that Apple still turned in a strong quarter despite offering fewer discounts and promotions than in past years.

Xiaomi held third place with 4.5 million units shipped, though its volume fell 15% year over year. Even so, the Omdia report said Xiaomi’s average selling price climbed 21%, driven mainly by record performance from the Xiaomi 17 and 15T series. That helped the company grow market value despite lower unit shipments, especially in France, Germany, and Spain.

Motorola posted 1.9 million units in shipments, up 17%, thanks largely to faster expansion in Spain and Portugal and continued progress in France and Italy. OPPO shipped 1.3 million units, up 9%, with growth tied to its return to France and gains in Romania and Poland. With realme and OnePlus now folded into its broader structure, OPPO is also reshaping its product mix and market strategy in Europe.

Honor ranked sixth and was the fastest-growing major brand, with shipments up more than 60% from the first quarter of 2025. Omdia attributed that jump mainly to Honor expanding its portfolio further into lower-priced segments.

The biggest headline in the study may be the region’s average selling price. Omdia principal analyst Runar Bjorhovde said Europe’s smartphone ASP reached 580 euros in Q1 2026, the highest level ever recorded. He linked that rise to a shrinking share of phones priced below 200 euros, which fell to a record-low 25% of total shipments, while premium demand stayed relatively solid, helped in part by Apple.

Bjorhovde also said the industry focus is shifting away from pure shipment volume and more toward value growth and sustainable operating results. Brands that once leaned heavily on mass-market models are increasingly pushing into the mid-range and premium tiers in hopes of attracting buyers who are less price-sensitive and more willing to upgrade.

Even so, Omdia’s outlook remains cautious. The firm said first-quarter results came in above expectations, but it still expects Europe’s smartphone shipments to fall 12% for full-year 2026, with much of that decline likely landing in the second half. As long as the market expects sharp future price increases, inventory levels may stay elevated. Over the medium term, though, Omdia believes a market pullback will be hard to avoid once memory prices begin to stabilize and inventory is brought down more carefully.